Retirement Planning

Our financial planning for retirement services are designed to help you navigate the financial, emotional and lifestyle challenges that come with retirement. We aim to give you the confidence to enjoy the retirement you’ve worked so hard to achieve.

Our financial planning for retirement process covers:

- Estimating the income you'll need for retirement, including healthcare costs and taxes

- Creating a long-term investment strategy for retirement

- Ongoing tax planning and strategies to reduce your taxes

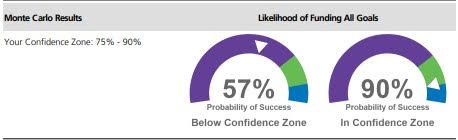

- Stress testing your plan to identify weaknesses, recommend improvements and predict how changes may impact outcomes

- Development of a tax-efficient income plan to cover your bills

- Recommendations on when to draw social security benefits

- Ongoing financial guidance and reviews

An effective retirement plan should be reviewed regularly and updated as needed.

Our process includes regular check-in meetings and calls to review your estate plans, insurance, tax strategies, and spending.

We’ll track your plan’s success rate, adjust for unexpected changes, and provide recommendations in plain English.

Want to see what YOUR retirement plan might look like? Click here to learn more about our retirement planning services.

Prudent Investment Management

A well designed retirement portfolio should balance the need for growth with the importance of preserving your assets and paying you income.

You should never work with an investment professional without knowing their investment “philosophy”. Here’s ours:

1) Own the right asset classes, at the right time.

According to Vanguard, 88% of your experience (the volatility you encounter and the returns you earn) can be traced back to your asset allocation.

That’s why we start with the big picture (asset allocation) before we get into the details (investments).

We do extensive research, attempting to own the right asset classes for the current environment. Our portfolios are tactical, seeking to take advantage of opportunities and mitigate risk we see in the market.

2) Utilize best-in-class investments and managers.

We prefer bundled products like ETFs to own asset classes we like, as they provide greater diversification than individual stocks or bonds.

Additionally, we believe that passive and active investments each perform better at different times, so our models include both in order to take advantage of their unique strengths.

3) Costs matter.

Research shows that a funds fee is a time-tested predictor of its returns. We agree, and we work to minimize investments fees for our clients.

The bottom line is that the less you pay for your investments, the more you keep in your pocket.

Our investment portfolios are built to help our clients navigate retirement. As a fiduciary in advisory relationships, our job is to make investment decisions that are in your best interest.

This means ignoring the noise and focusing on the data so we can select the right asset classes and best-in-class investments for our clients.

Want to learn more about building an investment portfolio for retirement? Click here to learn more about our investment management services.

All investing involves risk including loss of principal. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

Asset allocation does not ensure a profit or protect against a loss.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value, and may trade at prices above or below the ETF's net asset value (NAV). Upon redemption, the value of fund shares may be worth more or less than their original cost. ETFs carry additional risks such as not being diversified, possible trading halts, and index tracking errors.

Longevity Planning

Planning for a longer retirement starts with asking better questions.

Many retirees today can expect to live 25–30+ years after leaving the workforce. That’s great news—but it also makes retirement more complex. Longevity planning is about preparing not just your finances, but your life—for the long haul. This isn’t your parents’ retirement. You need a plan that covers more than just income.

What Longevity Planning Includes:

- Housing - Will you age in place, downsize, or relocate closer to family?

- Work - Will you fully retire, work part-time, or explore a second act?

- Independence - How do you maintain freedom and quality of life as you age?

- Health & Care - Are you prepared for rising healthcare costs or long-term care needs?

- Finances - Will your money survive 30+ years of spending, inflation, and unexpected changes?

Why It Matters

Longevity planning goes beyond traditional retirement advice. It’s about helping you:

- Stay independent longer

- Maintain flexibility as life changes

- Protect your health, home, and finances

- Make confident decisions for the decades ahead

Want to start building YOUR plan to support you through every stage of retirement? Click here to learn more about our longevity planning services.

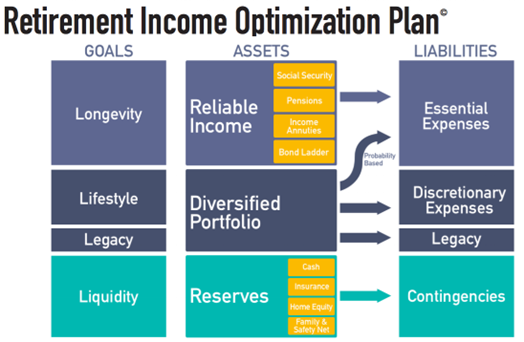

Preserve & Build Your Retirement Income

We can help you turn your savings and investments into income, so you can replace your salary. A good retirement income plan will:

- Keep your taxes low

- Cover fixed expenses with guaranteed income sources

- Provide the right balance between safety and growth potential

- Provide regular, monthly income during all market environments

Our income planning will consider all of your income sources, including social security, pensions, rental income, dividends, capital gains, annuities and required minimum distributions (RMDs).

Dr. Wade Pfau, Retirement Planning Guidebook

The goal is to build a reliable income plan that can change as your need for income changes, and is tax efficient. Remember, it's all about income in retirement!

Want to learn more about creating a tax-efficient income plan? Click here to get your free retirement assessment.

Tax Planning and Retirement

Taxes can become much more complicated in retirement.

Why?

Your income, once primarily from wages, may shift to sources like social security, pensions and annuities, investments, IRAs and Roth IRAs, dividends, rental properties and part time work.

Many of these sources are taxed at different tax rates while some aren't taxed at all.

Withholding the right amount can become complicated as your income changes year-to-year and you draw from different sources.

Our tax planning strategies aim to help you understand your taxes and keep them low. We do this by working with your tax advisor and considering strategies such as:

- An annual analysis of your tax return (View Example)

- Annual Roth conversions

- Coordinating of Income Streams to avoid "Tax Torpedoes" like Medicare IRMAA, AMT, and the Net Investment Income tax (NIIT) (Read More)

- Tax Loss Harvesting

- Charitable Giving Strategies like Qualified Charitable Contributions (QCDs)

We also stay up-to-date with tax laws to ensure you are taking advantage of every opportunity.

Want to learn more about minimizing your taxes in retirement? Click here to get your free retirement assessment.

Maximize Your Social Security

Choosing when to start Social Security is one of the most important decisions you will make in retirement. If you're married, it's even more important (and complicated).

The optimal time is different for every person because it's based on factors like your age, health, marital status and whether you are working.

It's important to make the right decision because Social Security is probably your most valuable source of income. That’s because:

- It's guaranteed by the US government

- It has a built-in cost of living adjustment (COLA) to help offset inflation

- It's taxed at a lower rate than most other income

As financial planning for retirement specialists, we will help you determine the best age to draw your benefits. We consider how it fits with other income sources you have like pensions, annuities, investments, or part-time work. We also consider special claiming strategies you may qualify for, such as:

- Spousal or widow's benefits

- Benefits from an ex-spouse

- Suspension of benefits

- Withdrawing your application

By reviewing your entire financial situation, we can recommend the right age for you (and your spouse) to draw your Social Security and help you maximize your benefits.

Want to learn which social security claiming strategy is right for you? Click here to get your free retirement assessment.