Mike Willaurer is a lead advisor at Compass Financial Group, where he brings decades of experience helping clients navigate the complexities of financial planning and market strategy. Known for his thoughtful insight and steady guidance, Mike provides clients with clear, practical advice tailored to their goals. Read on for his May 2025 Market Review.

May witnessed a notable market recovery, with the S&P 500 erasing its year-to-date declines. This encouraging performance unfolded amid evolving trade developments, varied economic indicators, and persistent questions about America's fiscal position.

Although numerous reports indicated economic strength, consumer confidence remained subdued regarding future prospects. Bond yields experienced volatility throughout the month as investors weighed federal spending and debt considerations.

For investors with long-term horizons, May demonstrates how markets can adjust to evolving circumstances, even amid substantial uncertainty surrounding economic and fiscal policies.

Primary Market and Economic Factors1

- The S&P 500 advanced 6.2% during May, marking its strongest monthly performance since 2023, while the Dow Jones Industrial Average climbed 3.9% and the Nasdaq surged 9.6%. For the year through May, the S&P 500 stands at 0.5%, the Dow at -0.6%, and the Nasdaq at -1.0%.

- The Bloomberg U.S. Aggregate Bond index dropped 0.7% in May yet maintains a 2.4% year-to-date gain. The 10-year Treasury yield concluded the month at 4.4%.

- Global equities also delivered solid returns, with both the MSCI EAFE index for developed markets and the MSCI EM index for emerging markets advancing 4.0%.

- The U.S. dollar index continued its decline, finishing the month at 99.3, approaching a three-year low.

- Bitcoin reached a fresh record peak of $111,092 before settling at $104,834 by month-end.

- Gold similarly achieved a new record high of $3,422 before closing at $3,288, representing a 24% year-to-date increase.

- May's Consumer Price Index data revealed consumer prices increased 2.3% year-over-year in April, the smallest 12-month rise since February 2021.

- April employment data showed 177,000 new jobs created while unemployment held steady at a low 4.2%.

Markets Demonstrated Resilience Amid Fresh Uncertainties

The May rally highlights the value of maintaining investment discipline during volatile periods.

Following April's setbacks, markets showed their adaptive capacity by recouping most losses and returning to positive ground in May. This recovery exemplifies how rapidly investor sentiment can improve when circumstances begin stabilizing, a dynamic witnessed repeatedly over recent years.

Naturally, historical performance cannot predict future results, and markets will likely continue grappling with trade developments, debt concerns, and economic health in upcoming months.

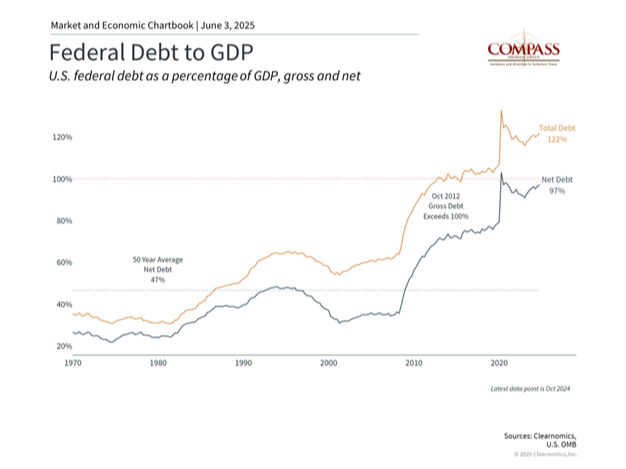

Moody's Reduced the U.S. Credit Rating

Among May's most notable developments was Moody's decision to lower the U.S. credit rating from Aaa to Aa1.

This action follows earlier downgrades by Fitch in 2023 and Standard & Poor's in 2011, all citing concerns about expanding debt and expenditures. The accompanying chart illustrates how U.S. total debt reached 122% of GDP in 2024. Net debt, excluding government obligations to itself, has climbed to 97%.

Despite the significance of this credit rating reduction, market reaction was minimal. This restrained response stems from the downgrade's retrospective nature, as investors already understand the nation's fiscal difficulties.

The subdued market impact also reflects experience from the 2011 Standard & Poor's downgrade, when Treasury securities maintained their status as preferred safe haven investments.

The timing of this downgrade coincided with House passage of extensive tax and spending legislation. The approved measure would preserve individual tax reductions from the Tax Cuts and Jobs Act. This encompasses a 37% maximum rate, child tax benefits, increased State and Local Tax deduction limits, and exemptions for tips and overtime compensation, among other provisions.

The Penn Wharton Budget Model estimates the legislation could expand deficits by $2.8 trillion over ten years.2 The Senate will now consider and potentially modify the bill.

While broad agreement exists that these fiscal issues need long-term resolution, the U.S. dollar maintains its position as the global primary reserve currency, ensuring continued Treasury demand for the foreseeable future.

Trade Discussions Advance Positively

May also brought meaningful trade negotiation progress, eliminating many extreme outcome scenarios.

The administration secured arrangements with both the U.K. and China, while continuing discussions with other significant trading partners. The U.S.-China agreement established a 90-day window of lowered U.S. tariffs on Chinese products.

Nevertheless, trade uncertainty will probably persist. Recent developments include mutual accusations between China and the U.S. regarding trade agreement violations, while the administration seeks elevated tariffs on steel and aluminum.

Simultaneously, European Union negotiations generated optimism when the White House postponed its planned 50% EU tariff following constructive talks. This indicates diplomatic resolution remains achievable, even when initial stances seem incompatible.

The administration also confronts legal obstacles to its tariffs. During May, the U.S. Court of International Trade invalidated numerous recently implemented tariffs, determining they surpass presidential authority under the International Economic Emergency Powers Act.

Although a federal appeals court suspended the ruling, maintaining current tariffs temporarily, this legal challenge introduces additional uncertainty to the trade environment.

Trade policy evolution typically spans months and years rather than days or weeks. May's recovery reminds investors to avoid overreacting to trade news, particularly as extreme scenarios have become less probable.

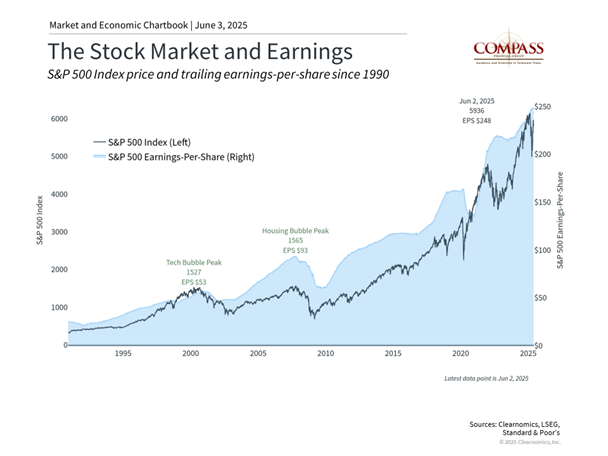

Consistent Earnings Growth Underpins Markets

First quarter corporate earnings provided additional optimism. S&P 500 companies achieved positive earnings per share surprises while 64% reported positive revenue surprises, per FactSet data.3

This robust earnings showing emphasized the fundamental strength of corporate profitability, with technology firms demonstrating resilience while managing trade uncertainties.

Conversely, consumers have maintained pessimistic outlooks this year due to tariff and inflation worries. However, recent sentiment measures began indicating improvement that better aligns with positive earnings and economic information.

The University of Michigan's latest May survey revealed slightly declining inflation expectations and stabilizing sentiment. While avoiding overinterpretation of single-month data remains important, this improvement represents encouraging progress. A robust economy combined with improving sentiment could provide market support.

The bottom line? May delivered positive results for investors. Although the U.S. credit rating downgrade and fiscal issues presented new obstacles, trade agreement progress helped elevate markets. For long-term investors, these events emphasize the importance of maintaining perspective and concentrating on fundamental trends rather than short-term policy developments.

- Standard & Poor's, Nasdaq, Bloomberg. All month end figures are as of May 30, 2025.

- https://budgetmodel.wharton.upenn.edu/issues/2025/5/23/house-reconciliation-bill-budget-economic-and-distributional-effects-may-22-2025

- FactSet Earnings Insight May 30, 2025

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

All performance referenced is historical and is no guarantee of future results.

All indices are unmanaged and may not be invested into directly.

All investing involves risk including loss of principal.

No strategy assures success or protects against loss.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio.

Diversification does not protect against market risk.

Stock investing includes risks, including fluctuating prices and loss of principal.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.