Mike Willauer is a lead advisor at Compass Financial Group, where he brings decades of experience helping clients navigate the complexities of financial planning and market strategy. Known for his thoughtful insight and steady guidance, Mike provides clients with clear, practical advice tailored to their goals. Read on for his Third Quarter 2025 Market Review.

Market volatility is an inherent aspect of the retirement investing journey, and 2025 has certainly demonstrated this reality. While downturns—including those triggered by trade policy developments—can feel unsettling, they often present chances to purchase assets at more favorable prices. Conversely, when markets rebound and set new records, some investors may experience anxiety despite solid fundamentals. In either situation, maintaining portfolios designed to endure all market cycle phases while keeping long-term financial objectives in focus becomes increasingly critical.

Entering the year's final quarter, investors confront mixed signals. During the third quarter, the S&P 500 achieved new record highs, buoyed by robust corporate earnings and artificial intelligence excitement. Simultaneously, labor market conditions have deteriorated noticeably since early summer, sparking concerns about economic fundamentals and consumer financial stability. Nevertheless, GDP growth has remained solid, and inflation has been relatively contained.

Such market conditions highlight the value of long-term retirement investing strategiesand financial planning. Instead of responding to news cycles and economic data releases, investors should maintain well-structured portfolios capable of adapting to market changes. This approach demands comprehension of the fundamental trends that will influence markets in upcoming quarters.

Key Market and Economic Drivers in Q3

- During the third quarter, the S&P 500, Nasdaq, and Dow Jones Industrial Average advanced 7.8%, 11.2%, and 5.2%, respectively, with all three establishing new records in September. For the year-to-date period, they have increased 13.7%, 17.3%, and 9.1%.

- The Bloomberg U.S. Aggregate Bond Index advanced 2.0% in the third quarter and has gained 6.1% year-to-date. The 10-year Treasury yield concluded the quarter at 4.15% after touching 4.02% in September.

- Developed market international equities (MSCI EAFE) climbed 4.2% while emerging market equities (MSCI EM) advanced 10.1% during the quarter.

- Gold surged to a new record of $3,841 per ounce, marking a 16% quarterly gain.

- Bitcoin finished at $114,641 for a quarterly gain, though it remains beneath its August high.

- The U.S. Dollar Index declined to 96.63 in September before closing at 97.78 for the quarter. Year-to-date, the dollar has weakened 9.9%.

- The Consumer Price Index rose 2.9% in August while core CPI increased 3.1%.

- According to the Bureau of Labor Statistics' latest report, only 22,000 net new positions were added in August. Since May, monthly job gains have averaged merely 26,800.

- During its September meeting, the Federal Reserve reduced rates by 0.25% to a range of 4% to 4.25%.

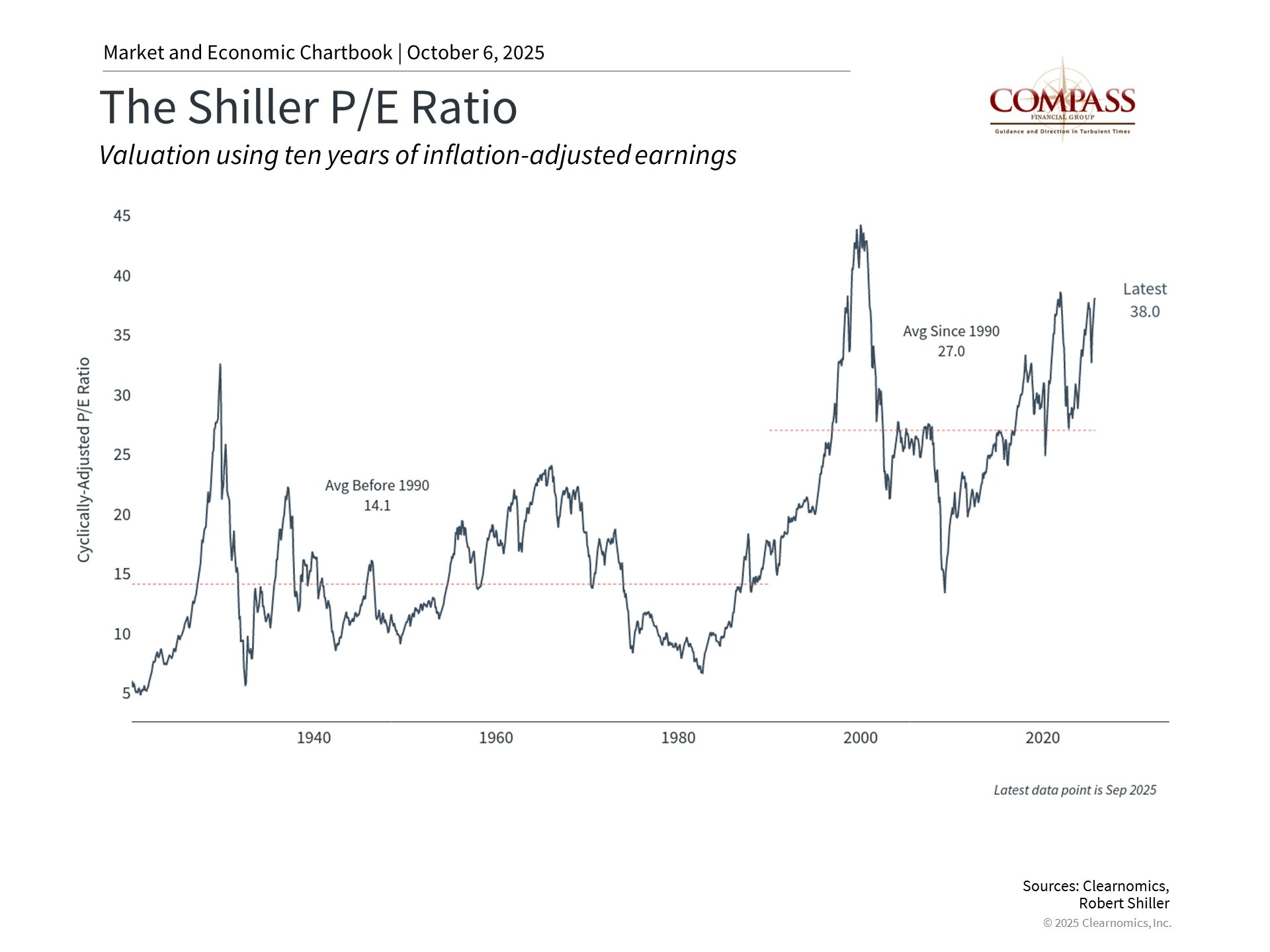

Market Valuations Approaching Historically Elevated Territory

For long-term retirement investing, overall market valuation levels represent a crucial consideration. Beyond simply examining market prices, valuations reveal what investors receive for those prices in terms of earnings, cash flow, sales, dividends, and other corporate fundamentals. While elevated valuations indicate investor optimism, they also suggest that expectations may be excessive in certain market segments.

The accompanying chart illustrates this through the Shiller price-to-earnings ratio for the S&P 500. The current reading of 38x substantially exceeds the 35-year average of 27x and approaches levels last observed during the dot-com bubble. This metric offers a longer-term view than traditional P/E ratios by utilizing a ten-year earnings history adjusted for inflation.

These valuation levels are unsurprising given the robust recovery over the past two quarters. Since April 8, the S&P 500 has surged 34%, producing a double-digit annual gain. Technology equities across multiple sectors have driven the market higher, just as they led it lower. The Magnificent 7 stocks, for example, have jumped 61% from the bottom. Although investors increasingly question whether corporate artificial intelligence spending will yield positive returns, this trend has been instrumental in driving broader market performance and business investment.

Valuations should not be viewed as short-term market predictors or timing instruments. Rather, they function as essential inputs for asset allocation decisions. While overall market valuations are high, this doesn't apply uniformly across all market segments. For instance, small-caps, value stocks, and international stocks currently offer more attractive valuations compared to large-caps, growth stocks, and U.S. stocks. This situation presents opportunities for investors with broader perspectives and extended time horizons—making it particularly well-suited for retirement investing.

Federal Reserve Lowering Rates as Employment Weakens

In September 2025, the Federal Reserve reduced interest rates by 0.25%, continuing its easing cycle after maintaining steady rates throughout much of the year. This action reflects the Fed's effort to balance persistent inflation above the 2% target against weakening labor market conditions. This rate reduction was broadly anticipated and has provided market support in recent months.

Several factors make this easing cycle distinctive. Traditionally, the Fed has reduced rates in response to economic crises or recessions. Although some weakness exists today, overall growth remains solid. Recent cuts therefore represent something different: an effort to normalize policy following the aggressive tightening cycle initiated in 2022. This explains why the Fed is easing policy even as the economy continues expanding and markets trade at record levels.

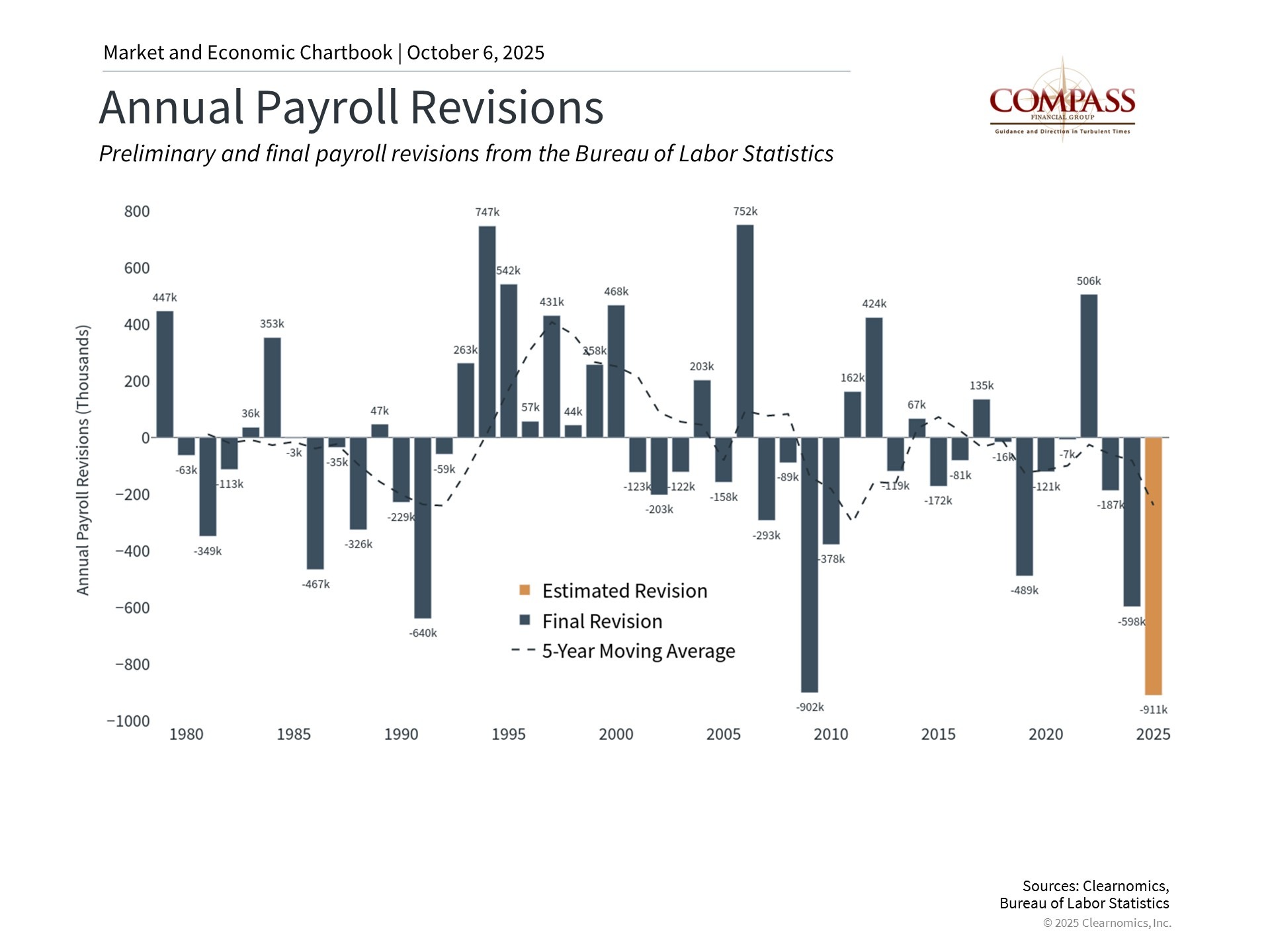

Job market deterioration has been the most significant factor influencing the Fed's decision. While the unemployment rate of 4.3% remains historically low, job creation has decelerated sharply. August added only 22,000 new payrolls, well below the 123,000 average from earlier in the year.

More striking are the payroll revisions indicating that 911,000 fewer positions were created over the twelve months through March than initially reported, as depicted in the chart above. The Bureau of Labor Statistics annually revises payroll figures based on more precise data than available during monthly reports. While these numbers remain preliminary, a revision of this scale would be historically unprecedented, revealing that labor market conditions have been weaker than previously understood.

Consequently, the Fed is reducing rates because, according to the latest FOMC statement, it "judges that downside risks to employment have risen." For investors, rate cuts generally support both equity and fixed income markets when economic conditions remain stable.

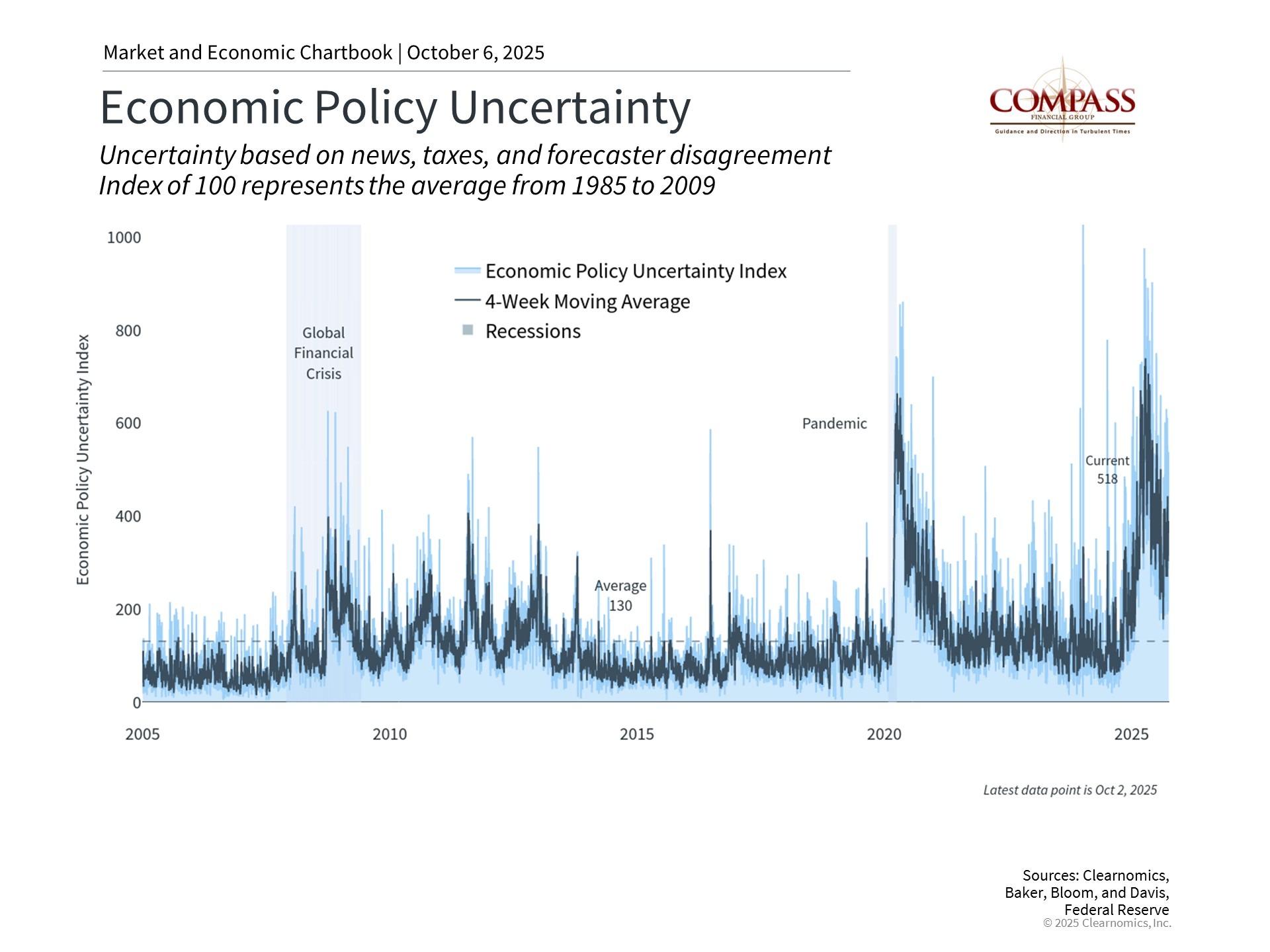

Policy Uncertainty and Market Volatility Currently Subdued

Following substantial volatility earlier this year driven by tariffs and tax policies, economic policy uncertainty measures have improved. The VIX index of stock market volatility stands around 16.3, beneath the long-run average of 18, while the MOVE index of bond market volatility has declined to 78, below the 87 average.

As many long-term investors recognize, calm market periods can shift rapidly. Recent years have witnessed numerous episodes of heightened volatility stemming from inflation, trade conflicts, Washington policy decisions, Federal Reserve actions, recession concerns, geopolitical tensions, and other factors. The current government shutdown represents merely the latest event potentially capable of disrupting markets short-term, even if long-term effects prove limited. Similarly, tariff policy outcomes and inflation impacts remain unclear.

While this uncertainty may feel uncomfortable for investors, it also drives long-term portfolio results. Recent years also illustrate the gap between investor fears and actual market performance. Rather than treating uncertainty as something to avoid, successful long-term retirement investing strategies recognize it as a market characteristic that creates opportunities to position portfolios for future years.

The bottom line? As we enter the year's final quarter, markets stand near record highs while economic signals remain mixed. This environment emphasizes the importance of maintaining suitable asset allocation and remaining focused on financial objectives long-term retirement investing objectives.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

All performance referenced is historical and is no guarantee of future results.

All indices are unmanaged and may not be invested into directly.

All investing involves risk including loss of principal.

No strategy assures success or protects against loss.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio.

Diversification does not protect against market risk.

Stock investing includes risks, including fluctuating prices and loss of principal.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.